Market Overview

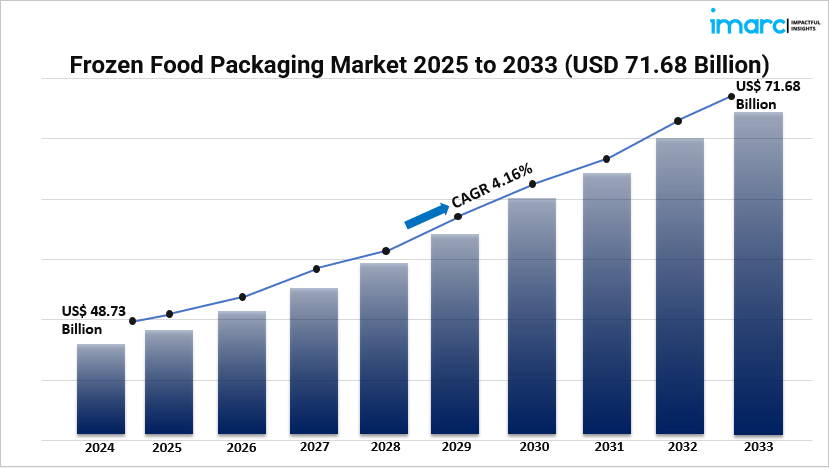

The global frozen food packaging market reached a valuation of USD 48.7 billion in 2024 and is projected to grow to USD 71.7 billion by 2033, exhibiting a CAGR of 4.16% during 2025–2033. This growth is propelled by increasing consumer demand for convenient, ready-to-eat meals, rising awareness of the nutritional value of frozen fruits and vegetables, and advancements in packaging technologies that enhance product shelf life and safety. Customized packaging solutions tailored to various frozen food types and sizes further contribute to market expansion.

Study Assumption Years

- Base Year: 2024

- Historical Years: 2019–2024

- Forecast Years: 2025–2033

Frozen Food Packaging Market Key Takeaways

- Market Size & Growth: The market was valued at USD 48.7 billion in 2024 and is expected to reach USD 71.7 billion by 2033, growing at a CAGR of 4.16%.

- Regional Dominance: Europe holds the largest frozen food packaging market share, driven by high demand for convenient meal options and sustainable packaging solutions.

- Product Segmentation: Ready meals dominate the product segment, reflecting consumer preference for quick and easy meal solutions.

- Material Preference: Paper and paperboards are the most preferred materials, aligning with the growing demand for eco-friendly packaging options.

- Packaging Types: Boxes are the leading packaging type, offering versatility and convenience for various frozen food products.

- Technological Advancements: Innovations such as vacuum sealing and modified atmosphere packaging (MAP) enhance product preservation and shelf life.

- Consumer Trends: Increasing awareness of food safety and hygiene, along with the convenience of online food delivery, are influencing packaging preferences.

Market Growth Factors

1. Technological Advancements in Packaging

Significant technical advancement is being made in the frozen food packing sector with inventions including modified atmosphere packaging (MAP) and vacuum sealing improving product preservation. By avoiding spoil and disease, these systems help to preserve the nutritional value and flavor of frozen foods and lengthen their shelf life. Furthermore increasing simplicity from microwave-safe and oven-safe packaging developments is cooking meals directly in the container. These developments not only raise food quality and safety but also address the increasing need for easy meal options.

2. Rising Awareness of Food Waste Reduction

Rising consumer worry about environmental sustainability is driving up demand for packaging options meant to reduce food waste. Clear labeling, resealable bags, and portion-controlled sizes help users use just what they need and properly store what they need for later eating. These packaging elements not only support a more sustainable future by aligning with consumer values but also help to battle food waste. Manufacturers are reacting by using environmentally friendly and biodegradable packaging materials, hence fueling market expansion.

3. Growing Demand for Sustainable and Eco-Friendly Packaging Materials

As awareness of the environment grows, customers are looking for packaging solutions that are environmentally friendly. Rising numbers of people are using recycled paperboard, compostable trays, and biodegradable films because of their lesser environmental effect. Manufacturers are embracing these environmentally friendly materials in order to attract environmentally conscious customers and show their dedication to sustainability. This change improves brand reputation and loyalty as well as helps the environment, therefore positioning businesses as progressive and responsible members of the industry.

Request for a sample copy of this report: https://www.imarcgroup.com/frozen-food-packaging-market/requestsample

Market Segmentation

Breakup by Type:

- Boxes: Offer versatility and strength, making them ideal for protecting a wide range of frozen products during transport and storage.

- Bags: Lightweight and space-efficient, suitable for various frozen food items.

- Cups and Tubs: Convenient for single-serve portions, commonly used for frozen desserts and snacks.

- Trays: Provide compartmentalization, ideal for ready meals and portion control.

- Wraps: Flexible packaging option for various frozen food products.

- Pouches: Offer convenience and are often used for frozen vegetables and fruits.

- Others: Includes innovative and specialized packaging solutions catering to specific frozen food requirements.

Breakup by Product:

- Ready Meals: Dominant segment due to consumer preference for convenient meal options.

- Meat and Poultry: Requires packaging that ensures freshness and prevents contamination.

- Sea Food: Packaging focuses on preserving delicate flavors and textures.

- Potatoes: Packaged to maintain quality and extend shelf life.

- Vegetables and Fruits: Packaging aims to retain nutritional value and freshness.

- Soups: Requires leak-proof and microwave-safe packaging solutions.

Breakup by Material:

- Plastics: Offer excellent barrier properties and flexibility, widely used in various frozen food packaging.

- Paper and Paperboards: Sustainable and biodegradable, aligning with eco-friendly initiatives.

- Metals: Provide durability and are often used for premium frozen food products.

- Others: Includes innovative materials like biodegradable films and compostable trays.

Breakup by Region:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Regional Insights

Europe dominates the frozen food packaging market, with more than 44% of the global share in 2024. This dominance is ascribed to the region’s great need for convenient meal alternatives, rising consumer awareness of food safety and hygiene, and a strong emphasis on sustainable packaging solutions. Innovations in eco-friendly packaging materials and designs are further propelling market growth in Europe.

Recent Developments & News

The frozen food packaging industry has witnessed significant developments aimed at enhancing sustainability and expanding market reach:

- Amcor acquired Bemis Company Inc., expanding its product portfolio and global presence.

- Berry Global announced the acquisition of RPC Group plc, broadening its product offerings and market reach, particularly in Europe.

- Cascades acquired Orchids Paper Products Company, strengthening its tissue paper business and presence in North America.

These strategic moves reflect the industry’s commitment to innovation, sustainability, and meeting evolving consumer demands.

Key Players

- Amcor plc

- Berry Global Inc.

- Cascades Inc.

- Crown Holdings Inc.

- Huhtamäki Oyj

- ProAmpac

- Smurfit Kappa Group plc

- Sonoco Products Company

- WestRock Company

Ask Analyst for Customization: https://www.imarcgroup.com/request?type=report&id=5293&flag=C

If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include a thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape, and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145