Homeowners hold a record $11.5 trillion in tappable equity, yet legacy banks still make them wait 30–40 days for a Home Equity Line of Credit (HELOC). Artificial-intelligence (AI) automation rewrites that script, collapsing decision times to minutes and funding timelines to five days while preserving rigorous compliance standards. This in-depth report—optimized for Yoast SEO with the focus keyphrase “AI-Powered Home Equity Lending”—explains the technology, market forces, consumer benefits, and regulatory safeguards that make digital HELOCs the breakout lending product of 2025.

Market Context: Record Equity Meets Digital Demand

Tappable equity hit a historic $11.5 trillion in 2024, with 32 million borrowers holding at least $100,000 each. At the same time, 82% of consumers now bank primarily online or via mobile, valuing speed and 24/7 access over branch visits. This convergence creates ideal conditions for AI-driven HELOC platforms that deliver instant answers and five-day cash.

How Traditional HELOCs Create Friction

Manual underwriting, in-person appraisals, and multi-layer credit reviews push legacy timelines out to 2–6 weeks. Borrowers submit paper documents, wait for appraisers, and endure committee queues—costing lenders money and homeowners time.

Comparative Timeline Table

The AI Decision Engine Explained

- Instant Data Aggregation – Secure APIs pull tri-merge credit, payroll deposits, and property records in seconds.

- Machine-Learning Risk Scores – Models trained on millions of loans predict default probability with 40% faster processing and higher accuracy.

- Automated Valuation Models (AVMs) – Desktop analytics replace 80% of full appraisals for qualified properties, cutting a week off cycle time.

- Real-Time Compliance Checks – Algorithms test every file against ECOA, TILA, and Reg Z triggers before issuing a decision, eliminating costly reworks.

Because two-thirds of tappable equity sits with 760-plus-score borrowers, most files are “clean,” allowing AI to approve within minutes while routing edge cases to human underwriters.

Consumer Benefits of AI-Powered HELOCs

Speed & Convenience

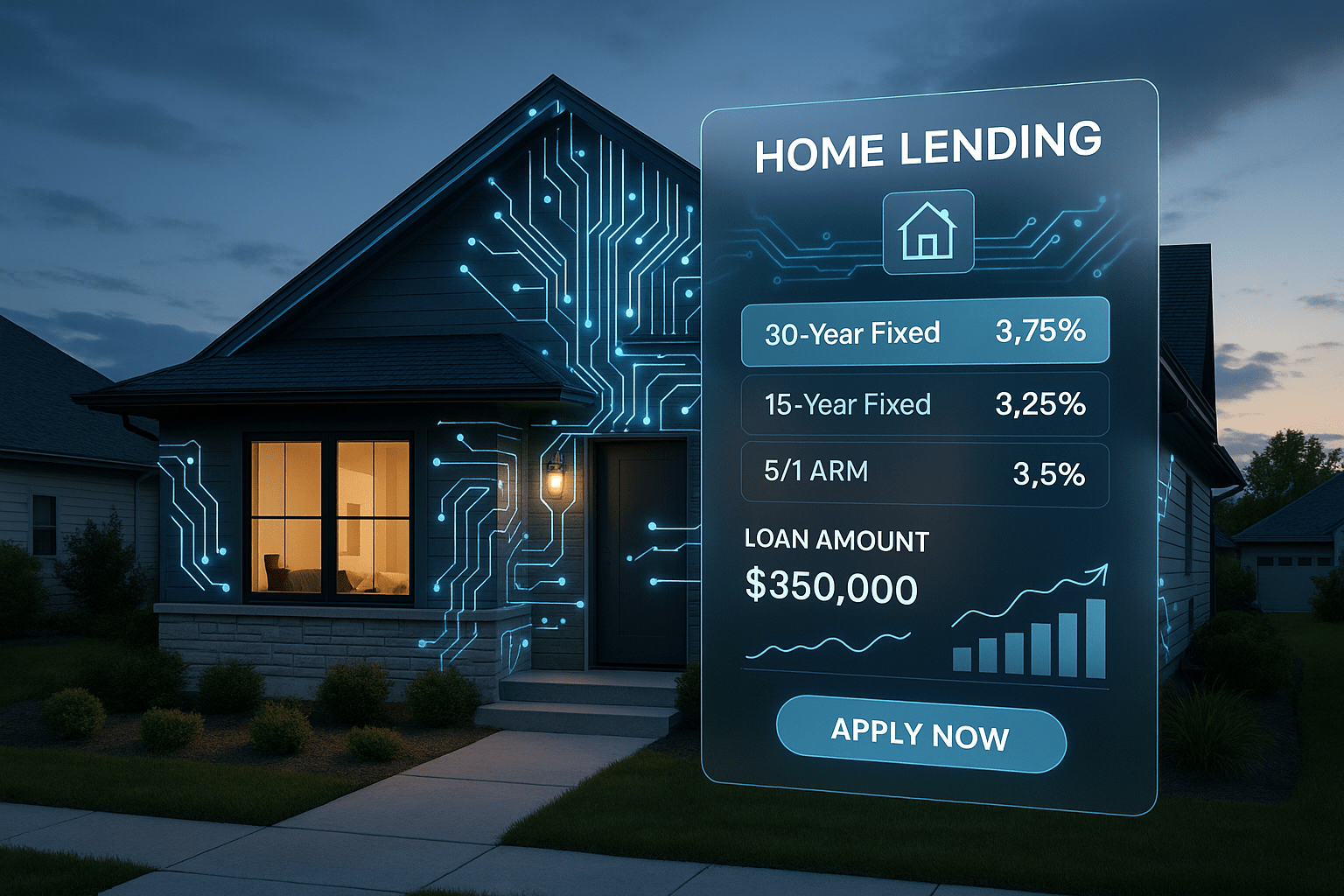

Borrowers receive conditional approval in under 15 minutes and funding in five days, matching renovation or debt-consolidation timelines.

Cost Efficiency

Automation slashes lender overhead, enabling competitive variable and fixed-rate draws without hefty origination fees.

24/7 Access

Digital portals let users apply, upload, e-sign, and draw funds anytime—meeting the 81% of consumers who bank daily online.

Inclusive Credit

AI models consider cash-flow data and alternative credit, helping thin-file or self-employed applicants secure lines traditional scorecards overlook.

Popular Use Cases

- High-ROI Renovations – Kitchen and bath upgrades boost home value and may keep HELOC interest deductible when funds “substantially improve” the property.

- Debt Consolidation – Replacing 22% credit-card APRs with single-digit HELOC rates can halve monthly payments for prime borrowers.

- Business Funding – Entrepreneurs tap equity for inventory or marketing instead of costlier merchant cash advances.

- Investment Property Leverage – Lines fund down payments, helping build rental portfolios without selling stocks.

End-to-End Digital Journey with HomeEQ

- Pre-Qualify in 2 Minutes – Enter basic data and receive a soft-pull estimate with no score impact. Start here: apply for HELOC online.

- AI Underwriting (≤15 Minutes) – Real-time decision disclosed; see performance metrics at online HELOC speed.

- E-Sign & Remote Notary – All disclosures completed on any device, satisfying Reg Z clear-and-conspicuous standards.

- Three-Day Rescission – Statutory cooling-off period for owner-occupied properties.

- Funding on Day 5 – ACH wires directly to your bank. Calculate payoff scenarios with the HELOC calculator.

- Flexible Draws & Rate Locks – Segment balances into fixed-rate tranches or keep variable access as market conditions dictate.

Compare personalized pricing anytime on the HELOC rates page.

Regulatory & Security Safeguards

- Truth in Lending Act (TILA) – Trigger terms like “APR” or “no closing costs” appear with equally prominent disclosures to prevent UDAAP issues.

- Equal Credit Opportunity Act (ECOA) – Bias testing ensures algorithms do not disadvantage protected classes; adverse-action letters cite specific data points.

- Gramm-Leach-Bliley Act (GLBA) – 256-bit encryption, least-privilege access, and SOC 2 audits protect borrower data.

- Fair Credit Reporting Act (FCRA) – Soft-pull inquiries during pre-qualification avoid score impact until final hard pull at closing.

Financial Impact for Borrowers

Economic & Industry Implications

Digital HELOC originations grew 64% in 2024, stealing share from banks whose legacy systems struggle to match five-day funding. As AI underwriting cuts processing costs by 40%, lenders can reinvest in customer acquisition or offer lower margins, intensifying competition.

Future Outlook: Instant Decisions & Same-Day Funding

Blockchain-secured e-notes and open-banking APIs will soon enable instantaneous lien recording and 24-hour disbursements once regulators modernize rescission rules. Expect further integration of real-time income verification and property-condition analytics, pushing home-equity access closer to a one-click experience.

Conclusion: Unlock Equity at the Speed of Life

AI-powered home equity lending aligns record homeowner wealth with the digital-first expectations of 2025. By automating every manual choke point, platforms like HomeEQ deliver approvals in minutes and funds in days while upholding strict regulatory and security standards. Whether you’re remodeling, consolidating debt, or scaling a business, an AI-driven HELOC transforms dormant equity into actionable capital—fast, flexible, and transparent.