Heavy Duty Trucks Market: Powering Global Commerce and Infrastructure Growth

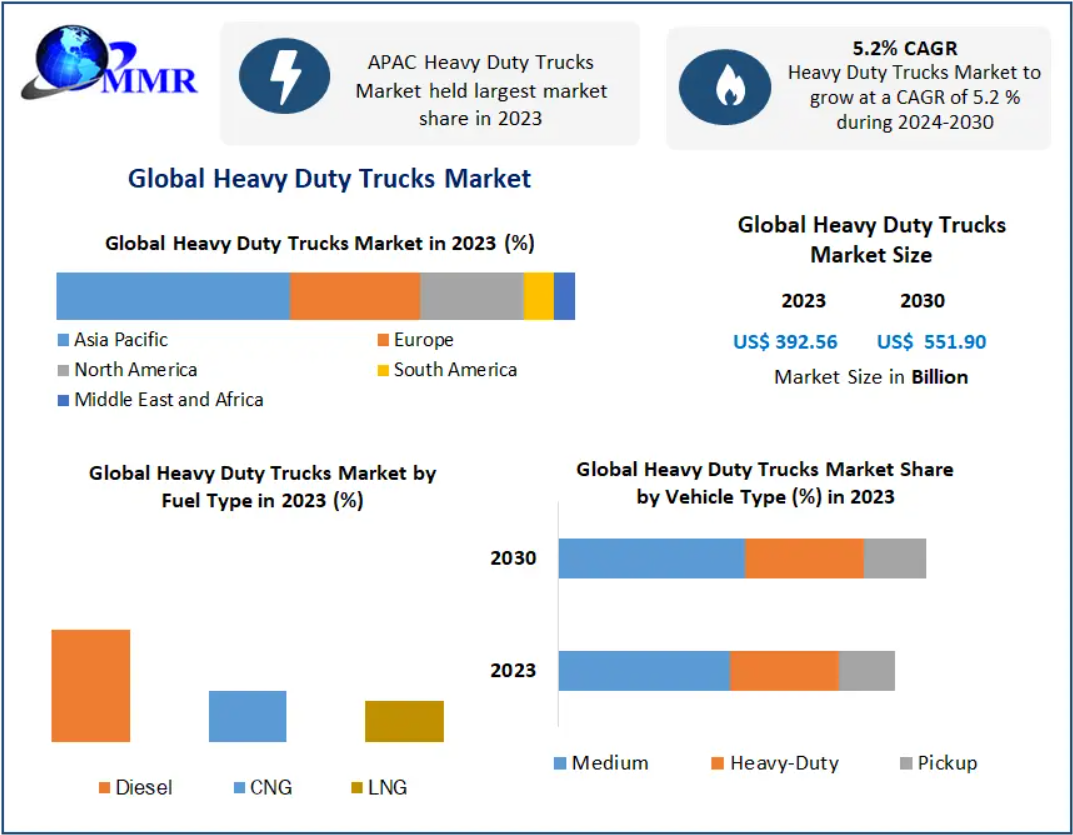

The Global Heavy Duty Trucks Market was valued at USD 392.56 billion in 2023 and is projected to reach USD 551.90 billion by 2030, expanding at a CAGR of 5.2% during the forecast period (2024–2030). The market’s growth is fueled by rising infrastructure investments, growing freight transportation needs, and the gradual shift toward cleaner, more efficient truck technologies.

Download a Free Sample Report Today: https://www.maximizemarketresearch.com/request-sample/12169/

Market Overview

Heavy-duty trucks—often referred to as heavy-duty vehicles or lorries—are essential assets in logistics, construction, agriculture, and industrial operations. Characterized by gross vehicle weights exceeding 33,000 pounds, these trucks are engineered to transport massive loads, from raw construction materials to finished goods.

Built with robust engines, reinforced transmissions, and multiple axles, heavy-duty trucks are indispensable to modern trade and infrastructure development. Their ability to haul over 20,000 pounds of cargo has made them vital for long-haul freight, mining, and construction site operations worldwide.

As global trade expands and developing nations intensify industrialization, demand for heavy-duty trucks continues to climb. Governments across Asia, Europe, and North America are heavily investing in road modernization and logistics networks, further amplifying market growth.

Market Dynamics

Key Drivers

- Surge in Infrastructure Development

Expanding urbanization and infrastructure initiatives—such as smart city projects and highway expansions—are driving the adoption of heavy-duty trucks. Emerging economies like India, China, and Brazil are witnessing rising investments in construction and logistics, boosting demand for high-capacity transport vehicles. - Shift Toward Electric and Hybrid Heavy Trucks

With stringent emission regulations from the European Commission (EC) and U.S. Environmental Protection Agency (EPA), OEMs are rapidly innovating. Leading manufacturers such as Tesla, BYD, Volvo, and Mercedes-Benz are introducing fully electric and hybrid heavy-duty models, reducing carbon footprints while meeting performance standards. - Expansion of Global Freight and E-Commerce

The surge in online retail and industrial manufacturing has significantly increased freight volumes. Heavy-duty trucks remain the backbone of road-based cargo transport, supporting both domestic and cross-border logistics.

Restraints

- High Initial Costs

The steep upfront investment required for heavy-duty and electric truck models remains a barrier, particularly for small and medium logistics operators. Base models are often marketed at lower prices, but buyers typically pay 30–50% more due to upgrades and custom configurations. - Environmental Concerns

Diesel-powered heavy-duty trucks emit nearly three times more carbon dioxide than gasoline vehicles, prompting stricter emission laws and a shift toward LNG and CNG alternatives. Manufacturers are now under pressure to develop low-emission, fuel-efficient solutions.

Download a Free Sample Report Today: https://www.maximizemarketresearch.com/request-sample/12169/

Market Segmentation Insights

By Vehicle Type

- Pickup Trucks:

Dominated the market in 2023 due to widespread adoption in North America, where pickup trucks serve both commercial and personal use. OEMs such as Ford and General Motors continue to develop fuel-efficient, high-performance models tailored for diverse applications including rescue, logistics, and personal mobility. - Heavy-Duty and Medium-Duty Trucks:

Expected to witness strong demand in construction, mining, and long-haul freight owing to their higher payload capacities and engine durability.

By Fuel Type

- LNG Segment:

Anticipated to record the fastest growth through 2030. Although LNG trucks are roughly 22% costlier upfront than diesel ones, their operating costs are about 40% lower, offering a 32% reduction in total cost of ownership.

The shift toward LNG is driven by cleaner emissions, supportive government policies, and projects like the J.B. Hunt LNG Truck Project in the U.S. - Diesel and CNG:

Diesel remains dominant in developing regions, while CNG is gaining traction due to lower operational costs and reduced emissions.

By Application

- Agriculture:

Held the largest market share in 2023. Heavy-duty trucks are indispensable in agricultural logistics—transporting fertilizer, fuel, livestock, and harvested crops to warehouses and markets. - Logistics and Distribution:

Expected to experience significant growth due to expanding trade routes and the increasing efficiency of road freight systems. - Construction, Tanker, and Special Applications:

High adoption in infrastructure, waste management, and fuel transport continues to propel these segments.

Regional Insights

Asia-Pacific (APAC):

APAC dominates the global market in both volume and value, accounting for the largest share in 2023. Countries like China, India, Japan, and South Korea are witnessing rising truck production and sales due to booming construction and logistics activities.

Regulatory reforms, stricter emission standards, and a shift toward premium and high-performance trucks are expected to accelerate regional market growth.

North America:

The U.S. remains a major hub for pickup and heavy-duty truck demand, with strong OEM presence including Tesla, Kenworth, Paccar, and Navistar. The region’s growing adoption of electric heavy-duty trucks aligns with clean energy targets and government incentives.

Europe:

Home to industry leaders like Volvo Trucks, Scania AB, Daimler AG, and MAN Truck, Europe’s market is driven by advanced engineering and sustainability goals. The continent is rapidly transitioning toward zero-emission heavy-duty fleets, especially in logistics and long-haul freight.

Rest of the World (RoW):

Latin America and the Middle East are emerging as promising markets due to infrastructure expansion and agricultural exports. OEMs are increasingly targeting countries like Brazil, Mexico, and South Africa for growth opportunities.

Download a Free Sample Report Today: https://www.maximizemarketresearch.com/request-sample/12169/

Competitive Landscape

The global heavy-duty truck market is highly competitive, with global OEMs focusing on technological innovation, modular design, and strategic alliances to enhance their market footprint.

Key Players Include:

North America:

Oshkosh Corporation, Navistar, Kenworth, Tesla Motors, Mack Trucks, Paccar Inc.

Asia Pacific:

TATA Motors, Ashok Leyland, Eicher Motors, Mahindra Motors, Hino Motors, Isuzu Motors, Mitsubishi Fuso, Dongfeng Motor Group, Hyundai

Europe:

Daimler AG, Ford Motor Company (Germany), Volkswagen, Scania AB, Volvo Trucks, MAN Truck, Renault Trucks, DAF Trucks, IVECO

These companies are actively investing in electric drivetrains, telematics, and autonomous driving technologies to meet evolving regulatory and market demands.

Future Outlook

The Heavy Duty Trucks Market is on the brink of transformation as it navigates the intersection of technological innovation, environmental sustainability, and logistics modernization. The integration of electric propulsion, telematics, and connected fleet management systems will define the industry’s next decade.

With global infrastructure spending rising and the logistics sector expanding, demand for durable, fuel-efficient, and intelligent heavy-duty trucks will remain robust through 2030. However, success will depend on how effectively manufacturers balance cost efficiency, sustainability, and performance in an evolving transportation ecosystem.

Conclusion

The Heavy Duty Trucks Market stands as a vital enabler of global trade, logistics, and infrastructure. While the transition toward cleaner fuel alternatives and electrification presents challenges, it also opens new growth frontiers for innovative OEMs and suppliers.

By embracing green technologies, digital integration, and modular design, the next generation of heavy-duty trucks will not only reduce emissions but also redefine efficiency and reliability in global transportation.